Tool -

Tool -

D2

Tool -

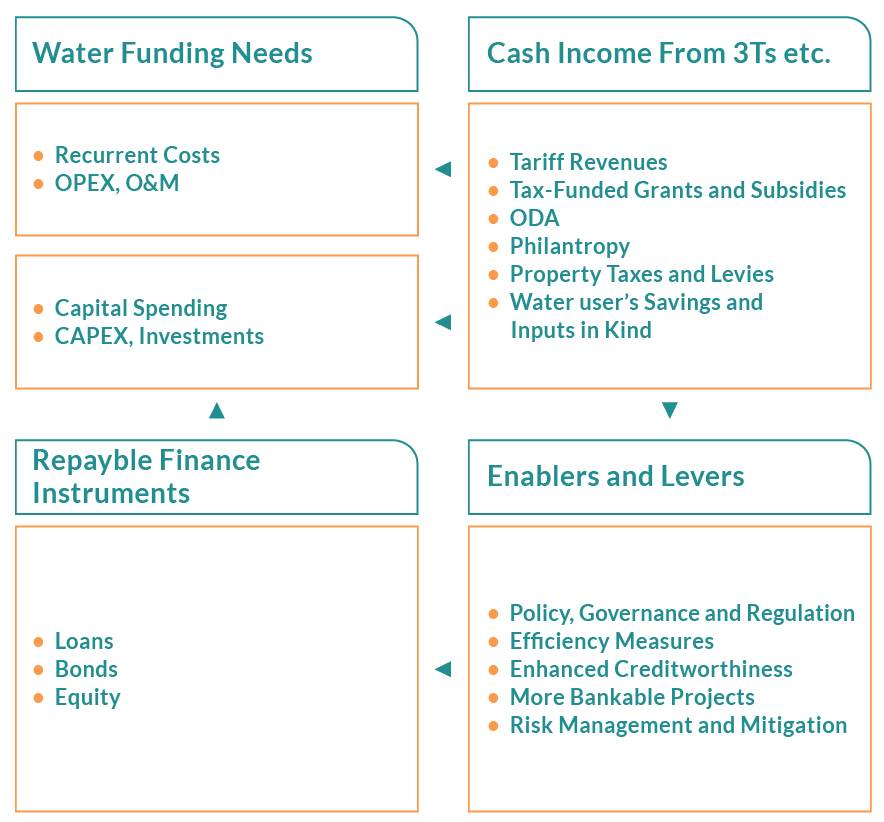

The term “investment” is generally used to describe the economic value creation processes in which productive assets yield benefits over a future period. In the water context, investment therefore also includes the funding and financing perspectives (Fig. 1). Funding corresponds to income or cashflows that water projects generate which mainly comes from “3Ts”, which stands for tariffs, taxes, and transfers (Tool D2.03). Financing, in turn, refers to accessing resources for capital investments and covering operational and maintenance costs which are paid back with funding sources. The choice of funding and the flows of financing depend on political environment, regulation framework, institutional arrangements, as well as conditions of capital markets. Funding and financing are mutually dependent when efficient finance reduces the funding requirement for water-related projects, and credible funding streams help secure low-cost finance (WWC and GWP, 2018).

Figure 1. Sources of funding and financing (Adapted from SWA, 2020).

The cost of this investment needs to be funded in various ways through private and public funds or a mixture of both – charging water users, investments from government budgets, and external aid. Most of the water infrastructure investment traditionally comes from the public domain. However, in recent times, there is a growing involvement of private commercial entities in sharing these costs (e.g., using water tariffs to protect watersheds through investment vehicles such as water funds).

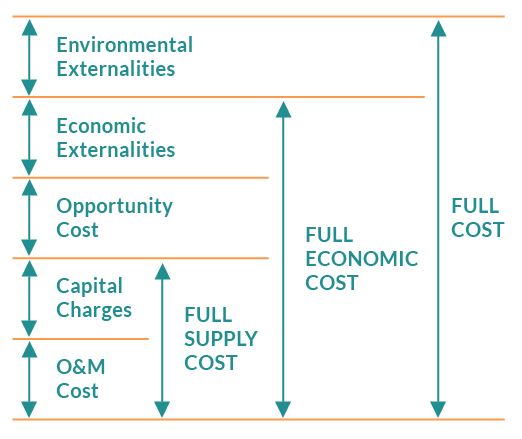

Stemming from one of the Dublin Principles that water is an economic good, the concept of full-cost recovery should be integrated into the decision-making of the water-related investment process. The full cost of providing water consists of the full economic cost and the environmental externalities, which are not easy to assign a monetary value to. Estimating the full economic cost may be the basis to start with, including full supply cost (operating and maintenance expenditures and capital charges), as well as the opportunity costs and the economic and environmental externalities (Fig. 2).

Figure 2. General principles for costing water (Adapted from Agarwal et al., 2000).

There is a need to ensure that water resources management agencies and water utilities have resources to be financially independent for them to reach the desired level of effectiveness. As a minimum, full supply costs should be recovered to secure sustainability of investment.

Dublin Principles state that water should also be taken as a social good, which generates social concern due to high supply costs. Marginalised populations whose incomes cannot afford to pay for full-cost recovery tariffs are in need of direct subsidies based on distributional decisions. Targeted subsidies need to take into account adequate revenue collection systems, mechanisms to identify the vulnerable groups, as well as the capacity to monitor and evaluate (Agarwal et al., 2000) – all of which are characteristic of a strong governance system.

Underinvestment in water is caused not only by a mismatch between finance and projects but also by the institutional instability, which hinders bringing about a favourable setting to obtain long-term returns for either public or private investors. Successful water projects with stable long-term flow of returns and high social outcomes depends on delicate institutional designs (Guerrero et al., 2016). Robust institutional arrangements and participation (Tools B) can protect consumers and investors, enhance efficiency, and help with risk sharing – all of which promotes the long-term financial sustainability in the water sector (Fig. 3).

Figure 3. Model of financing water supply and sanitation services. Source: WWC and OECD (2015).

Governance failure (Bakker, 2010) exposes water providers to political, economic, and social struggles that, in turn, increase the risk of investing in the sector. For example, a typical governance failure occurs when the institutional arrangements do not consider local economic, political, and cultural practices, generating negative incentives such as capture of public institutions, rent-seeking behaviour, and corrupt practices that undermine the efficiency and efficacy of WASH provision and, therefore, long-term returns for investors.

The last decade has witnessed a growing interest in reforming the water sector to attract more capital investments from public and private sources to achieve better water service provision, balanced allocation for multiple economic uses, and conserve natural ecosystems, and fight climate change. Recommendations on how to enhance opportunities for water sector funding and financing include (WWC and OECD, 2015, WWC 2018a; Heather et al., 2020; GWP and WWC, 2018):

The Tools in this Sub-section aim to provide insights on how to enhance funding and financing for water, including through: